While Private Equity (PE) has historically been one of the best performing asset classes for institutional investors, it remains under-allocated for most individual investors. In fact, while individual investors hold roughly 50% of the estimated $280 trillion of global assets under management (AUM), those same investors represent just 16% of the AUM held by alternative investment funds, including private equity, private credit and private real estate funds.[1] In addition to the high minimum investment required and the difficulties accessing these funds, a key driver of this under-allocation are the limitations of the traditional “closed-end” structure of private equity funds. Such limitations include: a) a lack of liquidity, b) less predictable cashflows, and c) a “cash drag” effect on investor returns, which arises from the burden on closed-end fund investors to manage their liquidity in order to satisfy somewhat unpredictable future capital call requirements – which ultimately dilutes the all-in investment return for individual investors.

At Nicola Wealth Management Ltd. (Nicola Wealth), we’ve created ways for our clients to invest in private equity without these traditional challenges. In this newsletter, we’ll discuss the key differences between an evergreen private equity fund such as Nicola Private Equity Limited Partnership (Nicola PELP) and a traditional closed-end private equity fund – and explain how the evergreen structure is generally better suited for individual investors. We’ll also touch on how one should think about, and compare, reported returns of both structures, given important differences in calculations.

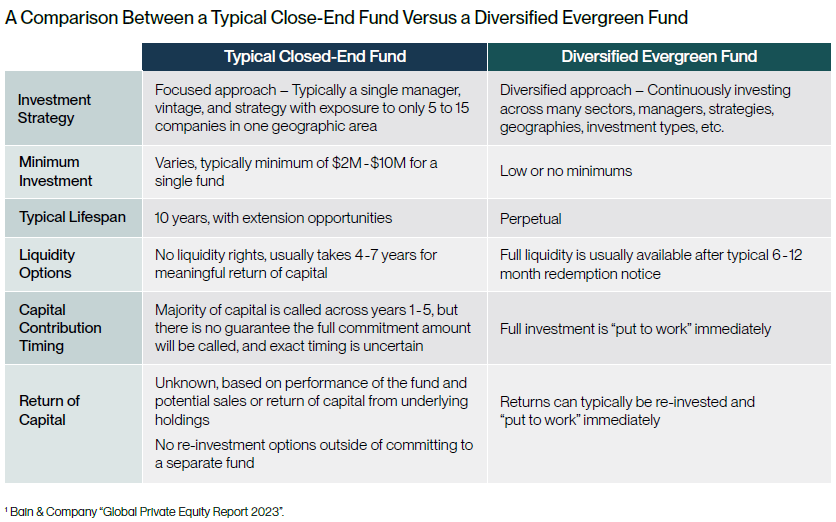

Liquidity

Traditional PE funds typically provide no liquidity option. This means investors have no discretion for when cash goes in and when cash comes out over the fund’s 10+ year life. In contrast, an evergreen structure like Nicola PELP’s, provides investors with more flexibility. For instance, purchases into the Nicola PELP can be made monthly while redemptions are subject to a 6 month notice period.

Money at Work

The traditional closed-end PE fund structure is based on investors making a “commitment” or pledging a certain amount of money upfront. However, not all the funds are put to work at the time of commitment; it is on standby for future “capital calls” made by the fund manager as new investment opportunities come up, typically over the first 4-5 years of the fund. Given that investors have little to no visibility for when this capital will be called, and with severe consequences for missing a capital call, this capital being held by investors for their fund commitment effectively becomes restricted capital that needs to be kept available on the sidelines either in cash or highly liquid, lower returning investments. This dynamic of closed-end PE funds creates a “cash drag” effect that dilutes the all-in investment return for individual investors.

The illustration shows how, in a traditional PE fund (right-hand side), only a portion of one’s commitment is actually at work at any point in time – on average it is close to half of one’s commitment; and that the other half is “restricted capital” – effectively held in liquid, lower returning assets. It’s important to note that, because of the contractual nature of capital calls, it does not make sense to invest restricted capital in risky assets that have any significant price volatility.

Similarly, when a traditional PE fund sells its underlying investments, it will distribute the cash proceeds to its investors. Timing of this distribution is also unpredictable and not at the discretion of investors. Investors will then have to re-invest this cash, taking on re-investment risk depending on the market environment and investment opportunities available at the time.

In contrast, evergreen PE funds such as Nicola PELP are nearly fully invested at all times and almost every dollar from the investor is put to work in a diversified portfolio earning private equity investment returns. For the Nicola PELP clients, there are no capital calls, restricted capital, or the need to reserve cash – once a dollar is invested, our clients are not on the hook for a penny more. All exit proceeds from the fund are automatically re-invested, allowing investors to stay invested and benefit from compounding effects, while removing the challenges around re-investing.

Investment Returns

Traditional closed-end PE funds calculate reported returns based on invested capital only – not on the commitment; ignoring the impact of the restricted capital and the “cash drag” effect of investors’ money on the sidelines waiting to be invested, and the money returned that may have re-investment risk. As a result, the all-in return to the individual investor can be perceived to be inflated. In comparison, evergreen funds calculate investment returns more holistically by considering the total commitment into the fund, thereby providing a better reflection of the all-in return to the investor.

Let’s look at an illustrative example of an investor making a $1 million commitment to a traditional closed-end PE fund with an internal rate of return (IRR) of 20%. By the end of year two, it’s common for a closed-end PE fund to have only called approximately 20% to 30% of the investor's commitment. Therefore, assume only $250,000 will be invested, while the remaining $750,000 will be held by the investor in a much lower-returning liquid investment or cash, waiting for the next capital call. As a result, the all-in return of the $1 million private equity investment for the investor is significantly less than the reported 20%.

To properly calculate and compare this all-in return, one needs to consider the lower and in some cases near zero return for the restricted capital waiting to be called by the traditional PE funds. A general industry rule of thumb is the reported IRR of a traditional closed-end fund needs to be ~2x that of an evergreen fund for it to be comparable on an all-in return to the investor basis.[3] As of March 31, 2024, the Nicola Private Equity Limited Partnership has generated a compounded annual return of 11.0% over the last five years. Applying this 2x rule of thumb, it is equivalent to a 22% IRR for a traditional closed-end PE fund.

Visibility, Certainty and Diversification

Traditional closed-end PE funds are sometimes known as “blind-pool” funds because investors have no visibility into what specific investments will go into the fund and when that will happen. Further, a lack of certainty and discretion over the timing of when the investments are made, and when this capital is eventually distributed back, creates an added layer of financial and tax planning challenges for investors.

In a diversified evergreen fund, in addition to the greater predictability of cash flows, there isn’t one large, concentrated position where a sale would have a material impact on one’s taxable income – which is beneficial for tax and planning purposes. Further, investors have a better visibility of what underlying opportunities their money is invested in at the time of investment.

Lastly, closed-end PE funds typically have a strategy that focuses on a specific region, sector, company size and maturity, and often have only ~10 underlying investments in each fund. The evergreen Nicola PELP has a multi-strategy PE portfolio across geographies and sectors in over hundreds of underlying businesses, providing our investors with significant diversification benefits.

With better liquidity, visibility, and diversification, we believe evergreen PE funds such as Nicola PELP are highly suited for individual investors to access and benefit from the opportunities of private equity as an asset class. When comparing the reported returns of evergreen funds and traditional close-end PE funds, an investor should fully consider the all-in returns of both structures, particularly the “restricted capital” requirements for a traditional PE fund investment and its dilutive impact on investment returns.

Disclaimer

This material contains the current opinions of the author and such opinions are subject to change without notice. This material is distributed for informational purposes only. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. This is not a sales solicitation. This investment is intended for tax residents of Canada who are accredited investors. Residency restrictions apply. Please read the relevant documentation for additional details and important. Past performance is not indicative of future results. All investments contain risk and may gain or lose value. Please speak to your Nicola Wealth advisor for advice based on your unique circumstances. Nicola Wealth Management Ltd. (Nicola Wealth) is registered as a Portfolio Manager, Exempt Market Dealer and Investment Fund Manager with the required securities commissions.

[1] Bain & Company, "Global Private Equity Report 2023".

[2] Partners Group, "Evergreen Funds: the next frontier for private markets investors". Traditional Closed End Fund cash flows are based on real historical figures from Cambridge Analytics and adjusted by Partners Group. For illustrative purposes only.

[3] JP Morgan Asset Management, "Apples Oranges and Best Practices", assuming the "restricted capital" is held in cash.

[4] Note: For a given Evergreen Fund’s time-weighted return figure (top row), the required equivalent return on a Traditional Closed End Fund to achieve the same dollar-on-dollar multiple (bottom row) is shown in the middle row.

[5] Partners Group, "Evergreen Funds: the next frontier for private markets investors". All returns shown are net of fees and expenses. Traditional Closed End Fund cash flows are based on real historical figures from Cambridge Analytics and adjusted by Partners Group. For illustrative purposes only.