For those with children or expecting, or perhaps with loved ones who are growing their families, you may be contemplating the best strategies to ensure these young individuals are positioned for long-term success. Although it may seem distant for new parents, in just 18 years, many children will seek higher education. With the escalating costs of post-secondary education, one of the most impactful steps you can take is to begin planning and saving for their educational future now. While the initial financial outlay for new parents can be significant, this article explores strategies to alleviate the future financial burden on both you and your children, should they choose to pursue advanced studies.

Registered Education Savings Plan

Many families are familiar with the Registered Education Savings Plan (RESP), which celebrates its 50th anniversary in 2024. Established to encourage Canadians to save for their children’s education, the RESP offers a valuable government contribution matching program under current legislation. This program provides a 20% government match on contributions, up to $500 annually. The lifetime maximum grant available is $7,200, with total allowable contributions capped at $50,000.

To maximize the annual grant, a contribution of $2,500 is required. Furthermore, if a child does not receive the full matching grants in a given year, the unused grant balance can carry over. This means you can catch up on prior grant years one year at a time. By contributing $5,000 annually, you can maximize the grant for the current year and catch up on one prior year.

Beyond the advantage of receiving government contributions, the RESP offers several compelling features for education savings:

- Tax Efficiency: Contributions, growth, and government grants within the RESP accumulate on a tax-deferred basis. When funds are withdrawn, the growth and grants are taxed at the child’s tax rate, which is typically lower. Contributions themselves are always withdrawn tax-free.

- Transferability: Should a child not utilize their RESP funds, both the growth and principal can be redirected to another blood-related child. Grants are also transferable among related children, though the total grant amount remains subject to each child’s lifetime maximum of $7,200.

- Income Splitting: The taxation on growth occurs in the hands of the beneficiaries (the children), potentially allowing for significant tax savings. Income that would otherwise be taxed at the parents’ higher marginal rates, up to 53.5%, is instead taxed at minimal rates, as most students have little or no income while pursuing higher education.

Funding Strategies

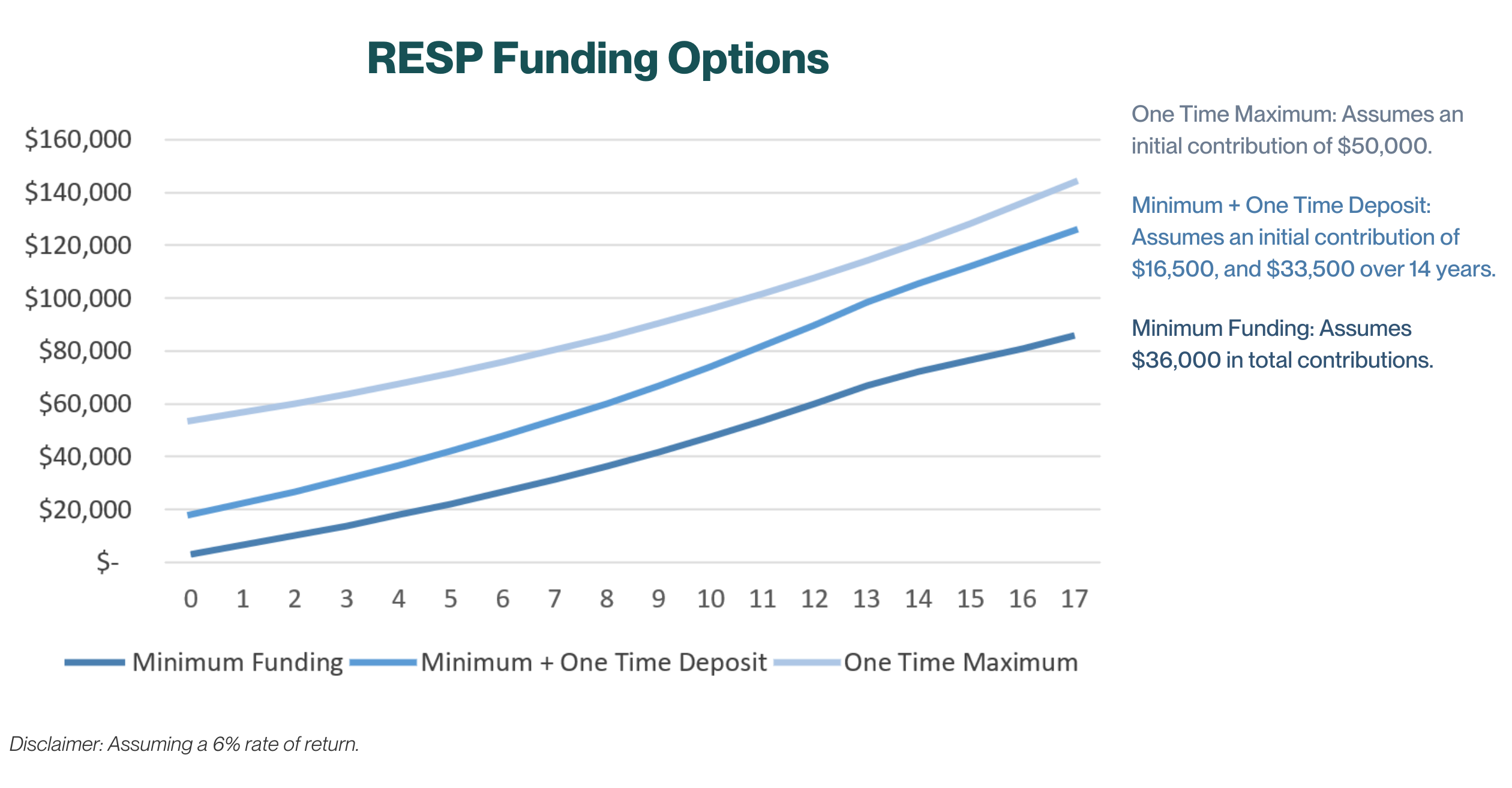

Many families choose to contribute just enough to their RESP to capture the full government matching grant, typically adding $2,500 annually to receive the $500 grant. Over the 18-year accumulation period, this strategy results in $36,000 in contributions and $7,200 in grants. Notably, this approach leaves $14,000 short of the lifetime maximum contribution limit of $50,000 per child.

But what if you could enhance the benefits of your RESP even further? Beyond securing the grants, additional contributions offer advantages like tax-deferred growth and effective income splitting.

Consider this: if you only contribute the minimum required to obtain the grants, and achieve a 6% annualized return, your RESP balance would reach an estimated $85,884 by the time your child turns 17. While this is a commendable amount, increasing your contributions could unlock even greater potential for growth.

To maximize government grants while contributing significantly to your RESP, consider making a one-time deposit of $16,500 when your child is born—comprising $14,000 plus $2,500. Following this initial deposit, continue with the minimum contributions required to secure the remaining grants, totaling $33,500 over the next 13 years. This strategy could yield a robust $125,844 by the time your child starts post-secondary education, nearly $50,000 more than if you only contributed enough to solely maximize the grants.

However, there’s an even more impactful approach if you have the funds available today. By depositing the maximum allowable amount of $50,000 into the RESP at the outset and letting it compound over 18 years, you would receive only $500 in grants in the first year. Despite this, you could amass an estimated balance of $144,144 by the time your child begins their post-secondary studies.

It's important to note that while funding the RESP to its maximum in the first year offers the potential for the highest return, this strategy's effectiveness could be affected by lower-than-expected or negative returns in the early years. The key advantage lies in the growth of the invested funds. Once the maximum contribution is made, additional investments cannot be made if market conditions are unfavourable.

Cost of Education

Now that we’ve explored strategies to maximize your RESP contributions, let’s consider what the cost of education might look like 18 years from now.

Currently, the average annual cost of tuition in Canada is $7,076, according to Statistics Canada. With an estimated annual increase of 3% in tuition fees, this amount will likely rise significantly by the time your child reaches post-secondary education. While $7,000 may represent the average, institutions like the University of British Columbia show a range from $6,000 to $10,000 per year for tuition alone. Additional expenses such as textbooks, food, and accommodations can add another $10,000 to $15,000 annually.

Looking ahead, the cost of a four-year degree in 18 years is estimated to range from approximately $40,000 on the lower end—based on $6,000 per year in tuition adjusted for a 3% inflation rate—to $170,000 on the higher end, which includes $10,000 in annual tuition plus $15,000 in additional expenses each year.

For students pursuing advanced degrees in fields such as law or medicine, costs can be significantly higher. Annual tuition for these programs may be double or even triple the average costs, and many professions require additional post-baccalaureate schooling, adding further financial considerations.

Withdrawals

Fast forward 18 years, and your child is ready to embark on their educational journey, perhaps dreaming of developing flying cars or finding solutions for global warming. How do you access the funds from the RESP?

In your child’s first term, you can withdraw up to $8,000 from the accumulated growth and grants in the plan. You can also withdraw any amount of the principal at your discretion. For subsequent years, there’s an annual limit of $28,122 (2024 amount) on withdrawals from growth and grants. It’s wise to manage the balance between taxable withdrawals (growth and grants) and non-taxable withdrawals (principal) to optimize tax efficiency. For instance, if your child earns $15,000 annually from a job and receives $15,000 in growth and grants from the RESP, their tax liability would be around $1,800 at an average rate of 9%. This amount could potentially be offset by tuition tax credits, possibly eliminating taxes owed. An experienced financial advisor can provide guidance on optimizing these withdrawals.

What if your child decides not to pursue post-secondary education? If you don’t have another child who can use the accumulated RESP funds, your options are:

- Close the RESP: You’ll receive your contributions back tax-free, but the grants will be returned to the government. The growth in the plan will be taxed in your hands, plus an additional 20% penalty on the growth attributable to government grants over 18 years.

- Transfer to your RRSP: You can transfer up to $50,000 of growth from the RESP to your RRSP tax-free. Any remaining excess will be paid out and taxed in your hands, with the 20% penalty applied. The grants will revert to the government, and your contributions will be returned tax-free.

In both scenarios, some amounts will likely be returned to the government in the form of grant repayments or taxes. Ideally, the RESP should be used as intended—to support your child’s education.

Overall, an RESP is an excellent tool for parents, grandparents, friends, and family to support children’s educational aspirations. While there are rules and regulations not covered in this article, consulting with a professional Wealth Advisor can help you navigate the plan and maximize its benefits. Early and consistent saving typically provides ample resources for your child to pursue their chosen education.

Disclaimer

This material contains the current opinions of the author, and such opinions are subject to change without notice. This material is distributed for informational purposes only. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. Nicola Wealth Management Ltd. (Nicola Wealth) is registered as a Portfolio Manager, Exempt Market Dealer, and Investment Fund Manager with the required securities commissions.